Quick answer

You’ve outgrown basic bookkeeping when your books are accurate, but they still can’t tell you what to do next. Bookkeeping, or “transactional accounting,” records what has already happened. It’s historical information. The moment you need your numbers to guide decisions, protect your cash, and keep you ahead of compliance, you need controllership: the layer of financial oversight that turns clean records into confident calls. If two or more of the signs below sound familiar, you’re there.

First, what “controllership” actually means

Most owners have never heard the word, so let’s make it plain.

A bookkeeper keeps your records accurate and up to date. A controller sits one level up and makes sure those records are reliable, compliant, and useful for running the business. That means owning your financial reporting, building internal controls so money can’t slip through the cracks, staying ahead of tax and filing deadlines, and translating the numbers into insight you can act on.

Think of it this way. Bookkeeping tells you what happened. Controllership tells you what it means and what to do about it. You can have great books and still be flying blind, and that gap is exactly what a controller closes.

We go deeper on that gap in Your Bookkeeper Keeps the Books. Who’s Actually Reading Them?

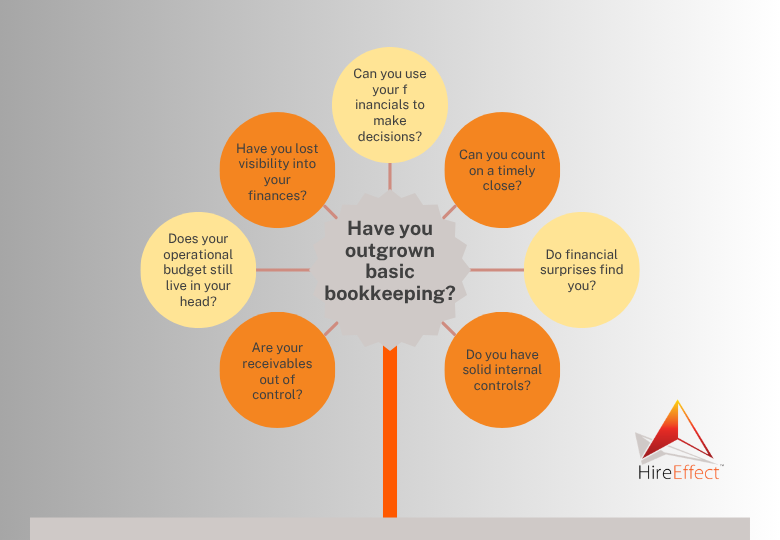

Here’s how to tell you’ve reached it.

1. You get reports, but you still can’t answer “Can I afford this?”

Your profit and loss statement lands in your inbox every month. It’s accurate. And you still can’t tell whether you can afford to hire, buy the equipment, or take the bigger space.

That’s the tell. Accurate records and decision-ready financials are not the same thing. When your reports describe the past but can’t guide the next move, you’ve outgrown bookkeeping. A controller builds reporting around the decisions you actually face, so the answer is in the numbers instead of in your gut.

2. You can’t count on a clean close at the same time each month

If your month-end numbers land at a different time every month, get revised after you thought they were final, or never really reach a clean close, you’re always steering with information you can’t fully trust. The problem isn’t the exact date. It’s that you can’t count on it.

A dependable monthly close, finalized in the same reliable window every month, is one of the clearest markers of financial maturity. A strong bookkeeping team builds that rhythm and tightens the process behind it. What controllership adds is oversight on top: a review layer that confirms the closed numbers are reliable, consistent, and ready to inform decisions, not just finished.

3. Surprises keep finding you

A tax notice you didn’t expect. A cash crunch that hit even though “business was good.” A deadline you learned about after you missed it.

Surprises are the most expensive way to run a business, and they almost always trace back to a missing layer of oversight. That layer exists to kill surprises before they cost you: monitoring compliance across sales tax, payroll tax, and franchise tax, watching cash flow before it tightens, and flagging risk while you can still do something about it.

4. One person controls the money from start to finish

If a single person can create a vendor, approve a payment, and send it out the door with nobody checking, you have a control gap. This isn’t about distrust. Good people in loose systems still make honest mistakes, and loose systems are where the rare bad actor hides.

This isn’t a rare problem. Small businesses lose a median of $141,000 to fraud, and more than half of those cases trace back to missing or overridden internal controls (Association of Certified Fraud Examiners, 2024 Report to the Nations). Internal controls, meaning simple checks so no one person owns a transaction end to end, are the fix. Most owners don’t think about this until something goes wrong. The whole point is to put the controls in first.

5. Accounts receivable is quietly becoming your problem

You made the sale. Getting paid for it has turned into a part-time job, and it’s yours. Meanwhile, the “we’ll pay you soon” balances keep aging.

Unmonitored receivables are cash you earned and can’t use, and every month one drifts, the odds it turns into bad debt climb. The median small business runs on just 27 days of cash buffer (JPMorgan Chase Institute), so every invoice that ages is a real squeeze, not a rounding error. A controller monitors receivables, tightens the collections process, and keeps small slippage from becoming a write-off. If you’ve become your own collections department, that’s a sign.

6. You’re budgeting in your head

There’s a number in your head for what the business should spend and earn this year. It lives nowhere else. No written budget, no plan to measure against, no early warning when you drift off course.

Running on a mental budget works right up until it doesn’t, and it fails fastest exactly when you’re growing, and the stakes are highest. That next layer brings an operating budget, spending and purchasing guardrails, and a way to catch overruns early. Structure isn’t bureaucracy here. It’s how you protect the freedom to make bigger moves.

7. Every growth milestone makes the finances messier, not cleaner

New location, new hires, new product lines. Each milestone you were proud of also made the books harder to trust and the month more chaotic.

That’s the loudest sign of all. Financial complexity grows faster than revenue does, and the systems that carried you to where you are now won’t carry you to where you want to go. When growth creates financial mess instead of financial clarity, you’ve outgrown basic bookkeeping, and it’s time for the next layer.

Quick self-check: Have you outgrown basic bookkeeping?

Count the ones that sound like you.

- Your reports are accurate, but they can’t tell you whether you can afford your next big move.

- You can’t count on a clean, final close at the same time each month.

- Financial surprises keep finding you, like a tax notice or a cash crunch you didn’t see coming.

- One person handles the money from start to finish, with no second set of eyes.

- Chasing unpaid invoices has quietly become your part-time job.

- Your budget lives in your head, not on paper.

- Every time you grow, the finances get messier instead of clearer.

One might just be a rough month. Two or more is a pattern, and that’s your signal it’s time to add a layer of financial oversight.

So what do you do about it?

Good news first: recognizing the signs is most of the work, and you don’t have to jump straight to a full-time hire.

Start by counting how many of the seven you nodded at. One might just be a rough month. Two or more is a pattern, and patterns don’t fix themselves.

From there, you have options. You can promote and train your bookkeeper if the talent’s there, hire a controller outright once the volume justifies it, or bring in a fractional controller [link -> https://hireeffect.com/fractional-controller-cost/], meaning senior financial oversight for a fraction of a full-time salary. For most owner-run businesses, fractional is the sweet spot: you get the expertise and the systems without carrying an executive salary before you’re ready.

The mistake we see most often is waiting for a crisis to force the decision. The whole value of controllership is that it prevents the expensive surprise, and you can’t prevent something that’s already happened.

Ready to close the gap?

If two or more of these signs hit home, let’s talk about what the right level of financial oversight looks like for your business. No pressure and no jargon, just a straight read on what you need and when. Reach out to our team and we’ll walk you through it.

Which of the seven felt the most familiar? That’s usually the best place to start.

FAQ

What’s the difference between a bookkeeper and a controller?

A bookkeeper records and maintains accurate financial transactions. A controller oversees those records to make sure they’re reliable and compliant, owns financial reporting and internal controls, stays ahead of tax and filing deadlines, and turns the numbers into insight you can act on. Bookkeeping tells you what happened; controllership tells you what it means.

How do I know if I’ve outgrown my bookkeeper?

The clearest sign is that your books are accurate but still can’t guide your decisions. Other signs include a month-end close that drags on too long, repeated financial surprises like unexpected tax notices, one person controlling money end to end, rising unpaid receivables, no written budget, and growth that makes your finances messier instead of clearer.

What are controllership services?

Controllership services are the financial oversight functions above day-to-day bookkeeping: financial reporting, regulatory compliance (sales tax, payroll tax, franchise tax), internal controls, budgeting and spend governance, and risk management, such as receivables monitoring. They turn accurate records into decision-ready financial information.

Do I need to hire a full-time controller?

Not necessarily. Many owner-run businesses use a fractional or outsourced controller, which provides senior financial oversight for a fraction of a full-time salary. It’s often the right fit for a business that has outgrown basic bookkeeping but isn’t large enough to justify a full-time executive hire.

When should a small business add controllership?

Ideally, before a crisis forces it. Common triggers include hiring your first employees, opening a second location, a growth spurt that complicates the books, or a compliance scare. Adding oversight at a milestone, rather than after a problem, is what lets controllership do its main job: preventing expensive surprises.